|

|

|

|

|

Restaurant Accounting: How to Accrue Payroll...and Why It's the Most Important Monthly Task You are Ignoring!By John Nessel

The first time I heard anyone use the accounting terms "accrue" and "accrual", I had a mild panic attack. But, trust me... it is really not a hard concept to grasp. More importantly, by taking the concept of accrual into account, you can produce a monthly Profit and Loss Statement that is infinitely more accurate, especially as it relates to your payroll costs. To accrue payroll is simply to recognize that the end of a weekly or bi-weekly payroll does not usually coincide with the end of the month, and therefore an "accrual" is necessary to recognize those payroll expenses that occurred in the current month that otherwise would not be recorded till the following month. Don't fret, we will explain by example in short order.

First off, why is there a need to do anything at all as it relates to your payroll entries into QuickBooks? The answer is simple. If you are like 99% of restaurant owners or operators, you are evaluating your financial performance based on a "monthly" profit and loss statement. On the other hand, you are most likely processing your payroll on a weekly or bi-weekly basis. The math is straightforward...most months will consist of 30 or 31 days of revenue and corresponding expenses, but will only account for 4 weekly or 2 bi-weekly payrolls, in both cases representing only 28 days. You are therefore regularly understating your true payroll cost by 7-10%. If you process payroll every two weeks, then two months each year will include an extra payroll, and in those months your total payroll costs will be grossly overstated by as much as 40%!

Now, human nature being what it is, the ten months of understated payroll are ignored, and you, the owner, remain in a state of blissful denial. Then of course the extra payroll months appear, and the typical reaction is to casually dismiss the result as being overstated without ever similarly recognizing the other ten months of under-reporting. Sound familiar?

Simply put, the process of accruing payroll is designed to eliminate this problem. By accruing payroll each month your Profit & Loss Statement will reflect an equal number of revenue, expense and payroll days. As payroll expenses typically constitute over 30% of every restaurant revenue dollar, an accurate accounting of payroll is critical.

We will use a typical payroll scenario to take a look at how this works. Assume that you are 1) processing your payroll on a weekly basis, 2) each payroll period begins on a Monday and 3) checks are distributed Friday's for the period ending the prior Sunday.

Using Jan 2004 as an example, the last payroll of that month (that is the last payroll that included days in January) was not processed until Friday Feb 6. That means that while the checks were dated Feb 6, the actual pay period covered was Monday Jan 26 through Sunday Feb 1. So while the payroll will be recorded on the day the checks are cut (Feb 6), six of the seven days of the payroll actually occurred in January. The process of accruing January payroll involves recognizing those six payroll days (Jan 26-31) in the month of January by making a Journal entry that records them as a January expense. In order not to double count these six days both in the January "accrual" entry and when you record the full payroll on February 6, we need to "reverse" the accrual entry on the first day of February.

To determine the proper dollar amount for an accrual entry you need to divide the number of days to accrue (six for the month of January) by the total number of days in the payroll period (seven for a weekly payroll). Multiply this percentage (6/7= 85.7% for January) by each payroll expense line item in your normal payroll journal entry to arrive at the proper allocation to be accrued for that month. Then make a "General Journal" entry dated the last day of January to record the accrual by Debiting the Payroll Expenses and Crediting a Liability Account to be named "Accrued Payroll". This entry is then "reversed" on the first day of February. (Note: QuickBooks Premier Edition actually has a feature that automatically reverses a General Journal entry to save you the time of having to do it manually.)

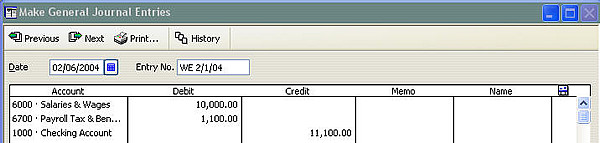

In the most basic case using a single General Ledger account for wages and another for employer payroll taxes, here is what these Journal entries would look like. The first journal entry simply records the Feb 6 payroll while the second and third journal entries reflect the payroll accrual and then the reversal of the payroll accrual.

#1. Last Payroll of the Month That Includes January Wages. Note that it is dated Feb 6 because that is the day the payroll checks are processed even though the pay period is from Monday Jan 26-Feb 1, 2004.

#2. Accrual Entry. (Note Jan 31 Date). Accrue the portion of the Feb 6 payroll (85.7% of the total payroll expenses shown in #1 above) that accounts for the last six days of January wages by Debiting the Wages and Salaries and the Employer Payroll Tax accounts and Crediting the Accrued Payroll Account. These payroll expenses will now be recognized in January, the month they actually occurred.

#3. Reverse Above Accrual Entry. (Note Feb 1 Date) This steps accomplishes two tasks. First it makes sure that you do not double count the six days of payroll accrued above in #2. Second, it establishes the actual number of paydays of the Feb 6 payroll which will be recorded in February. In this case is the number of days equals one (seven days from the original payroll entry #1 minus six days from the Feb 1 reversal below)

In summary, we have used the the last payroll in the month that includes January paydays (the payroll processed on Feb 6), and the proper number of days that need to be accrued (six days representing Jan 26-31), and thereby created a Journal entry dated Jan 31 to recognize these January payroll expenses that would not otherwise be recorded until February. To prevent these expenses from being "double counted" when the Feb 6 payroll is recorded, we have reversed the accrual as of Feb 1. This also has the effect of starting the next month (February) with an accurate payroll total that "nets" the Feb 6 payroll (a full seven days) against the Reversal entry of Feb 1 (negative six days) which accurately reflects the fact that the Feb 6 payroll really only included a single day in that month, Feb 1 (remember that payroll was actually for the period from Jan 26-Feb 1.). I know i assured you that this would not be too difficult to understand....perhaps I exaggerated a bit, but i assure you that if you can follow this procedure at the end of each month you will reap huge benefits in having an accurate Profit and Loss statement as it relates to Payroll.

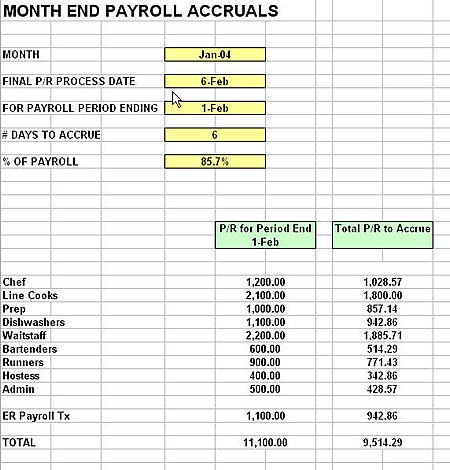

As a final suggestion you might want to make the Journal entry calculations easier by creating a Template in Microsoft Excel (see below) which lists all your Wage & Employer Tax GL accounts in a column. In the next column enter the actual dollar amount for each payroll expense account from the Payroll to be used to make your accrual (in this case the Feb 6 payroll). Determine the percentage of the total payroll to be accrued by dividing the number of days to accrue by the total number of days in the payroll period (either 7 or 14). Now, multiply that percentage by each rows payroll total to yield the total payroll dollars to accrue for each line. Use these numbers to make your accrual journal entries in QuickBooks (both the accrual and the reversal).

More Restaurant Accounting & Restaurant Finance Articles...

|

|

John Nessel is the President of

John Nessel is the President of